5 Year Cds Spread Definition

Cds Spreads As A Measure Of Risk Le Blog De Ufm Team

Sovereign Cds Q A Bond Vigilantes

Credit Default Swaps Cds

The Credit Default Swap Market What A Difference A Decade Makes

Understanding Credit Default Swaps Pimco

:max_bytes(150000):strip_icc()/CorporateBonds_CreditRisk22-8c12f1dbc1494f28b3629d456fb4fa63.png)

Corporate Bonds An Introduction To Credit Risk

These bonds usually offer a higher yield than government.

5 year cds spread definition. Cds value changed 2 48 during last week 13 74 during last month 5 37 during last year. This value reveals a 0 26 implied probability of default on a 40 recovery rate supposed. The buyer of the cds makes a series of payments the cds fee or spread to the seller and in exchange may expect to. A credit default swap spread is a measure of the cost of eliminating credit risk for a particular company using a credit default swap.

This page provides vietnam credit default swap historical data vietnam cds spread chart vietnam cds spread investing and data. The united states 5 years cds value is 15 7 last update. The basis is the difference between the spread over the risk free rate on a bond issued by a government and corporate and the cds spread. A credit default swap cds insures against losses stemming from a credit event.

A credit default swap cds is a financial swap agreement that the seller of the cds will compensate the buyer in the event of a debt default by the debtor or other credit event. When cds spreads widen it is a bearish signal and the stock prices of the firm typically. That is the seller of the cds insures the buyer against some reference asset defaulting. In other words the spread is the difference in returns due to different credit qualities.

5 oct 2020 17 45 gmt 0. For example if a 5 year treasury note is trading at a yield of 3 and a 5 year corporate bond corporate bonds corporate bonds are issued by corporations and usually mature within 1 to 30 years. Between cds spreads and the information they reflect about reference entities has become weaker during the recent years in which cds activity has declined. The five common variables that affect cds spread include the equity market s implied volatility industry leverage of the reference entity the risk free rate and liquidity of the cds contract.

The changes in cds spreads also affect the stock prices. Vietnam 5 year cds spreads are an indicator of the market current perception of vietnam default risk. A higher credit default swap spread indicates the market believes the company has a higher probability of being unable to pay investors which means it would default on its bonds. As a simple example greek 5 year bonds yield 440 bps over similar maturity german government bonds risk free hopefully and the cds is at 400 bps.

Current cds value reached its 6 months minimum value.

How To Read Cds Prices Featuring Portugal Ft Alphaville

Understanding Credit Default Swaps Pimco

Https Onlinelibrary Wiley Com Doi Pdf 10 1002 Fut 21828

/idata%2F3271534%2Fcds1.png)

Cds Spreads As A Measure Of Risk Le Blog De Ufm Team

A Security Guard Protects An Eleven Year Old Girl Who Is Being Targeted By A Gang For Participating As A T Data Science Infographic Data Science Data Scientist

When Do Cds Spreads Lead Rating Events Private Entities And Firm Specific Information Flows Sciencedirect

The Rise Of Collateralized Synthetic Obligations Beware The Rhyme Of History Guggenheim Investments

Liquidity In Credit Default Swap Markets Sciencedirect

Radiohead 2 2 5 Radiohead Hail To The Thief Music Pictures

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcroqr8 Jw5kgbolcgtkuh4mcgm34q F Jrbxg Usqp Cau

Credit Default Swaps Cds Intro Video Khan Academy

Skye Mastercard Allows You To Convert Purchases Of 250 Or More To Your Choice O Credit Ca With Images Credit Card Online Credit Card Website Credit Card First

:max_bytes(150000):strip_icc()/dotdash_Final_Line_of_Credit_LOC_May_2020-01-b6dd7853664d4c03bde6b16adc22f806.jpg)

Line Of Credit Loc Definition

:max_bytes(150000):strip_icc()/dotdash_Final_Introduction_To_Counterparty_Risk_Feb_2020-02-5477c45c30ee48b4b09617f3b88300f4.jpg)

Introduction To Counterparty Risk

Procyclicality In Tradeable Credit Risk Consequences For South Africa

Sovereign Debt Banks And Firms Investment In Italy Vox Cepr Policy Portal

/CurrencySwapBasics-effa071aba184066b9683bf80750c254.png)

Currency Swap Basics

Do Banks Still Monitor When There Is A Market For Credit Protection Sciencedirect

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gct5umyzanrpm0rhbywgikdlydmfwfmg3i4zx220sxs 8fgmbtg7 Usqp Cau

Pdf The Valuation Of Credit Default Swap Options

A Guide To The Five Lands Of Italy Quranmualim Learn Islam Learning Drives Learn Islam Learn Quran Listen To Quran

Https Www Moodysanalytics Com Media Article 2016 Cds Implied Edf Measures Fair Value Cds Spreads At A Glance Pdf

How U S Structured Finance Has Changed Since The Credit Crisis S P Global Ratings

Children Education And Development Health Education Health And Nutrition Education

The Fed Banking System Conditions

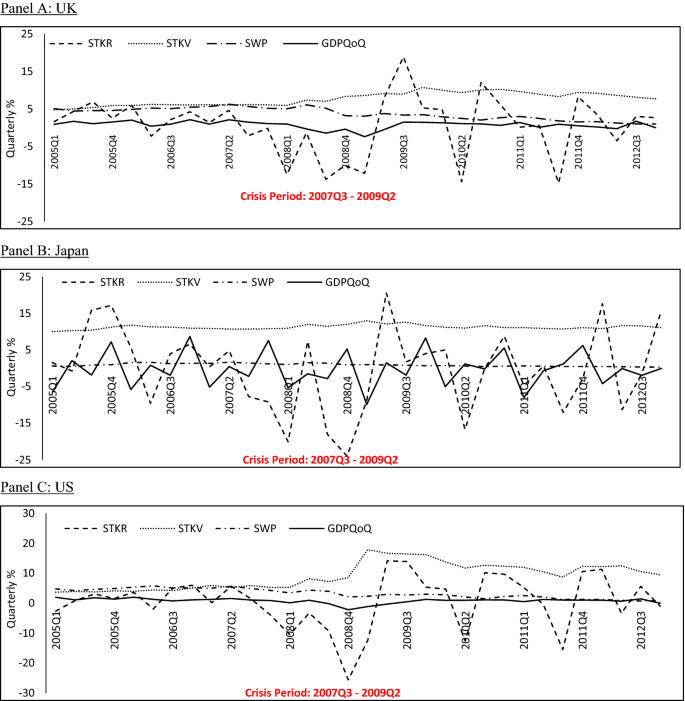

Credit Default Swap Spreads Market Conditions Firm Performance And The Impact Of The 2007 2009 Financial Crisis Springerlink

The Generation Between Gen X And Gen Y Call Us The Xennials Generation Generations Quotes Generational Differences

Exodus From Sovereign Risk Global Asset And Information Networks In The Pricing Of Corporate Credit Risk Lee 2016 The Journal Of Finance Wiley Online Library

Fantasy Faire Magic Music Festival Jefferson Airplane The Doors Grassroots Iron Butterfly Cou Music Festival Poster Music Concert Posters Concert Posters

Political Uncertainty And A Firm S Credit Risk Evidence From The International Cds Market Sciencedirect

Do Your Little Dinosaurs Have A Case Of The Wiggles Have Them Stand And Follow Preschool Songs Dinosaurs Preschool School Songs

Https Www Actuaries Org Uk Documents F9 Credit Hedging Good Bad And Ugly

Https Www Moodysanalytics Com Media Article 2020 Weekly Market Outlook Coronavirus May Be Black Swan Like No Other Pdf

Pin On Bathroom And Laundry Love

Midi Hits Backing Music For Musicians Singers Faqs Midi In 2020 With Images Music Download Karaoke Cds Free Mp3 Music Download

Pdf Estimating Market Implied Recovery Rates From Credit Default Swap Premia

Mental Fitness Challenge Boxed Set Bullet Journal Workout Bullet Journal 30 Day Challenges Bullet Journal 30 Days

Christian 60th Wedding Anniversary Cards Zazzle Com Anniversary Card For Parents Wedding Anniversary Cards Anniversary Cards

Unofficial Designs Joseph Novak Pastor Designer Church Music Liturgy Songs

Table Of Content 1 Introduction Of Business Essentials Business Ethics 2 Business Ethics Business Essentials Ethics Meaning

Dad Personalized Pocket Pillow Father S Day Gifts Gifts Etsy In 2020 Unique Gifts For Dad Christmas Presents For Dad Funny Gifts For Dad

Credit Default Swaps Part I Of Iii A Brief History Of Mechanics Product Types And Standardization Seeking Alpha